Q4 2021 HPI shows growing availability of homebuyer assistance programs for first responders and other community heroes

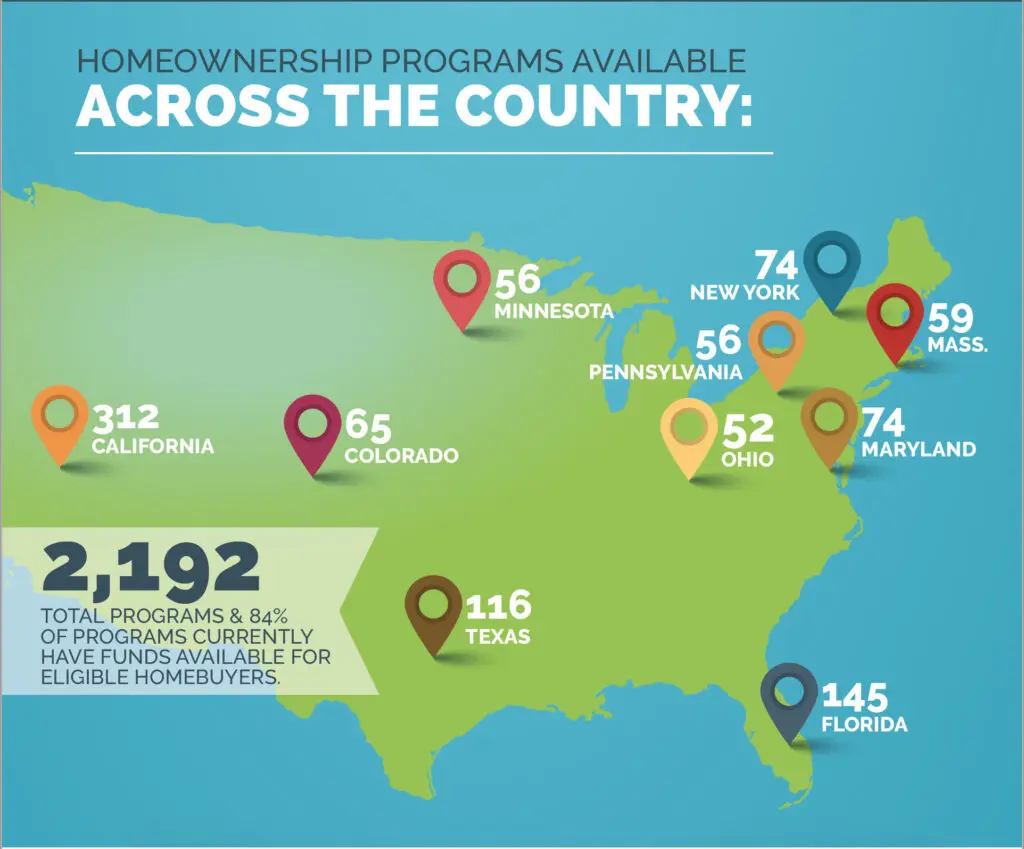

The Q4 2021 Homeownership Program Index (HPI) covers 2,192 programs across the United States, of which 83.6% had funds available for eligible homebuyers as of January 6, 2022 (up nearly 2% from the previous quarter).

Breakdown by Program Type

73 percent of programs in the database are for down payment or closing cost assistance.

63 percent of all DPAs include payment deferral for some period of time.

43 percent of all DPAs are partially or fully forgivable.

38 percent of all DPAs are both deferred and forgivable.

11 percent of programs are first mortgages.

5 percent of programs are Mortgage Credit Certificates (MCCs).

11 percent are additional programs, including matched savings programs and Housing Choice Vouchers (HCV).

Spotlight: Special Incentives for Heroes

This quarter’s report highlights the increasing number of homebuyer assistance programs designed to benefit teachers, first responders, law enforcement officers, firefighters, healthcare workers, and other providers of critical community services. These programs accounted for nearly 9% of all homebuyer assistance programs available in Q4. Another 11% of programs offer benefits for veterans, members of the military, and surviving spouses.

Homebuyer programs with special incentives for community servants have been available in markets across the country for decades. These can be standalone programs or provisions that add special benefits or more flexible eligibility requirements when community heroes apply for homebuyer programs that are also open to other applicants. Program providers may structure these programs to help encourage homeownership in a revitalization area, help community heroes to live close to where they work, and help recruit and retain key service personnel. To qualify for a homeownership program, both the buyer and the property must meet certain criteria, which will vary by program.

Here are some examples of homebuyer programs available to community heroes in Q4 2021:

The CalHFA MyHome program offers a deferred-payment loan to assist with down payment and/or closing costs with a cap of $15,000. CalHFA will waive the $15,000 loan amount cap for qualified CA fire department employees and CA school employees.

The Washington State Housing Finance Commission (WSHFC) Veterans Down Payment Assistance Loan Program enables qualified Washington State veterans to receive up to $10,000 to help with down payment assistance.

New York veterans can take advantage of the State of New York Mortgage Agency (SONYMA) Home for Veterans (HFV) program. This program is available to active service members, veterans, and their spouses or co-borrowers and offers up to $15,000 in down payment assistance.

The Jefferson Parish Finance Authority (JPFA) Heroes to Homeowners program offers a $2,500 non-repayable grant for education professionals, first responders, healthcare professionals, veterans, and active military personnel.

The Utah Housing Corporation (UHC) Veteran First-Time Homebuyer Grant is for members of the military or veterans who separated in the last five years and are first-time Utah homebuyers. The program offers up to $2,500 in down payment help and does not require repayment.

The Tennessee Housing Development Agency (THDA) Homeownership for the Brave program provides special benefits to veterans and members of the military, such as a reduced interest rate and no first-time homebuyer requirement.

Community heroes may also benefit from special savings and rebates from Homes for Heroes when they buy, sell or refinance a home.

Other key findings from the Q4 2021 report include:

Funding levels are on the rise. 84% of programs had funds available for eligible homebuyers. That level of funding reflects a nearly 2% increase from Q3 2021.

Three out of four programs (73%) focus on helping homebuyers with down payments and/or closing costs. This figure includes repayable, partially forgivable, and fully forgivable programs. Other major categories of assistance include affordable first mortgage programs (11%), Mortgage Credit Certificates (5%), matched savings programs, and Housing Choice Vouchers.

Assistance is available for repeat homebuyers and landlords. Approximately 38% of programs do not have a first-time homebuyer requirement. In addition, 27% of programs allow buyers to purchase a multi-family property as long as the buyer occupies one of the units.

Availability varies by location. Three out of four (74%) programs are targeted to properties in specific locales such as cities, counties, or neighborhoods, with the balance of programs available statewide through state housing finance agencies. The states with the most homebuyer assistance programs are California, Florida, and Texas.

Support for manufactured housing is increasing. While homebuyer assistance programs have historically favored site-built homes, as of Q4, 28% of programs allow manufactured housing as an eligible property type, up nearly 2% from the previous quarter.

Methodology

Published quarterly, DPR’s HPI surveys the funding status, eligibility rules, and benefits of U.S. homebuyer assistance programs administered by state and local housing finance agencies, municipalities, nonprofits, and other housing organizations. DPR communicates with over 1,200 program administrators throughout the year to track and update the country’s wide range of homeownership programs, including down payment and closing cost programs, Mortgage Credit Certificates, and affordable first mortgages, in the DOWN PAYMENT RESOURCE® database.